Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

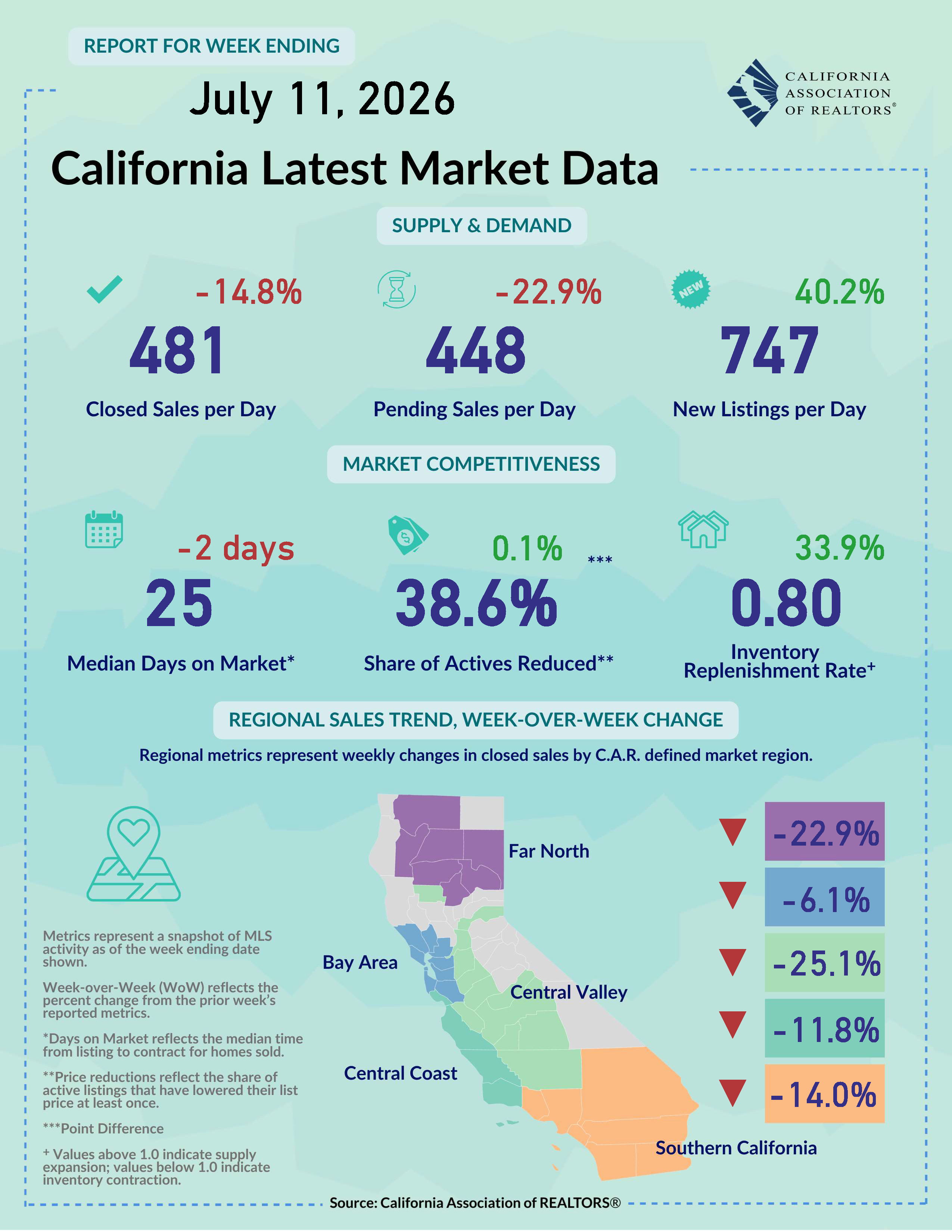

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle sits down with former Senate Majority Leader Emeritus Robert Hertzberg to discuss the proposed Middle-Class Homeownership and Family Home Construction Act.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

July 13, 2026 - Despite housing market conditions remaining lackluster through the first half of 2026, the market is showing some promising signs as the second half gets underway. Mortgage rate-lock activity rose sharply in June, suggesting that more buyers may be reentering the market as rates moderate, while younger buyers continue to account for a growing share of purchase activity. Combined with renewed policy attention on housing supply and affordability, these early indicators offer cautious optimism that sales momentum could improve in the months ahead. Landmark housing legislation becomes law on Friday: The 21st Century Road to Housing Act – the largest housing affordability bill in decades – became law over the weekend as President Trump decided neither to sign or veto the bill on July 10th. The legislation is packed with nearly 50 individual housing measures ranging from corporate homeownership to manufactured home construction. The bill is designed to modernize existing federal housing programs, improve the effectiveness of affordable housing initiatives, and encourage greater housing production. Key provisions in the new housing law includes an establishment of a $200 million grant pool to incentivize municipalities that remove restrictive zoning laws, the creation of a HUD pilot program designed to increase the availability of small-dollar mortgages and bans on institutional buying that prevent Wall Street firms and major corporate investors from purchasing single-family homes en masse. The passing of the bill represents a major step forward in addressing our nation’s housing affordability and supply challenges. Home sales expected to pick up as rate locks rise: Despite softer-than expected market conditions in the first half of 2026, U.S. home sales are expected to climb in the next couple months as mortgage rate locks jumped to the highest level since 2023, according to Optimal Blue’s June 2026 Market Advantage report. Total mortgage rate-lock volume, a leading indicator of home sales, was up 10% from May and up 14% from last June. Elevated mortgage rates have kept many would-be buyers on the sideline in the first half of the year, but moderations throughout last month prompted buyers to reenter the market. A separate study released by Intercontinental Exchange, Inc. shows that young buyers continued to gain market share despite affordability challenges, with Gen Z accounting for one in five purchase rate locks in Q2 2026, the largest share on record. The generation now makes up almost one-third of all first-time buyers’ mortgages and more than a quarter of FHA purchase lending. With many more Gen Zer’s entering their prime age of homebuying, their presence in the market will grow further in the years to come. Americans value neighborhood walkability: The 2026 National Association of REALTORS® (NAR) Community and Transportation Preference Survey found that Americans continue to place a strong value on walkable, mixed-use neighborhoods that provide easy access to parks, shops, restaurants, and everyday services. Nine out of ten (89%) of respondents said sidewalks and places to walk are important when deciding where to live, while eight out of ten (82%) valued being within walking distance of parks and shopping. Two-thirds (63%) said they would be willing to pay more to live in a walkable community, and 59% preferred a smaller home lot in a walkable neighborhood over a larger property that requires more driving. The survey also revealed broad support for expanding housing choices, including small-lot single-family homes (63%), townhomes, duplexes, and other attached housing options (51%). Overall, the findings suggest that demand for compact, amenity-rich communities remains strong and could support policies that promote housing diversity, infill development, and transportation accessibility. Remodeler sentiment in the West slips to negative territory for the first time in six years: Remodeling market sentiment at the national level remained positive but turned negative for the West region in the second quarter, according to the latest National Association of Home Builders (NAHB) Remodeling Market Index (RMI). The RMI dipped one point to 61 in the latest quarter but stayed above 50, a level that indicates more remodelers view conditions as good than poor. Current market conditions remained steady with large remodeling projects dipping three points while moderate remodeling projects climbed four points. Future indicators softened again for the second straight quarter, however, as both leads/inquiries and backlogs inched down from the previous quarter. Rising costs and lingering economic uncertainty were major headwinds that keep remodeler sentiment down in the recent quarter. Nearly three quarters (74%) of respondents, in fact, reported that prices of materials have increased by an average of 6.7% since Q1 because of higher fuel costs. At the regional level, RMI improved the most in Northeast (+11 points) while the West (-6 points) had the biggest drop, slipping below 50 for the first time since Q1 2020. With prices of building materials not likely to return back to pre-war levels in the current quarter, remodeling sentiment could remain stagnant – particularly in the West – if mortgage rates do not show more consistent downward movement in the coming months. Short-term inflation expectation inches up but optimism on employment outlook rises: Inflation expectations at the one-year ahead horizon increased slightly last month after dipping briefly in May, according to the New York Fed’s Survey of Consumer Expectations. Respondents collectively expected inflation 12 months from now to reach 3.7% - the highest level since September 2023, despite gas price growth expectations falling to the lowest level since August 2022. The medium-term inflation expectations also inched up by 0.2 percentage points (ppts) but were unchanged for the longer-term inflation expectations. On a more positive note, consumers felt more upbeat about the labor market in June as their perceived probability of losing one’s job in the next 12 months decreased by 1 ppt to 14.1%, while the perceived probability of finding a job if one’s current job was lost increased by 1.2 ppts to 44.9%. With recent job reports showing consistent growth in the past few months, labor market expectations started showing improvement as economic uncertainties begin to ease. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

|